Oct 30, 2023

Circular Manufacturing: A Sustainable Path to the Future

Circular manufacturing or circular economy is defined as a production and consumption model whereby …

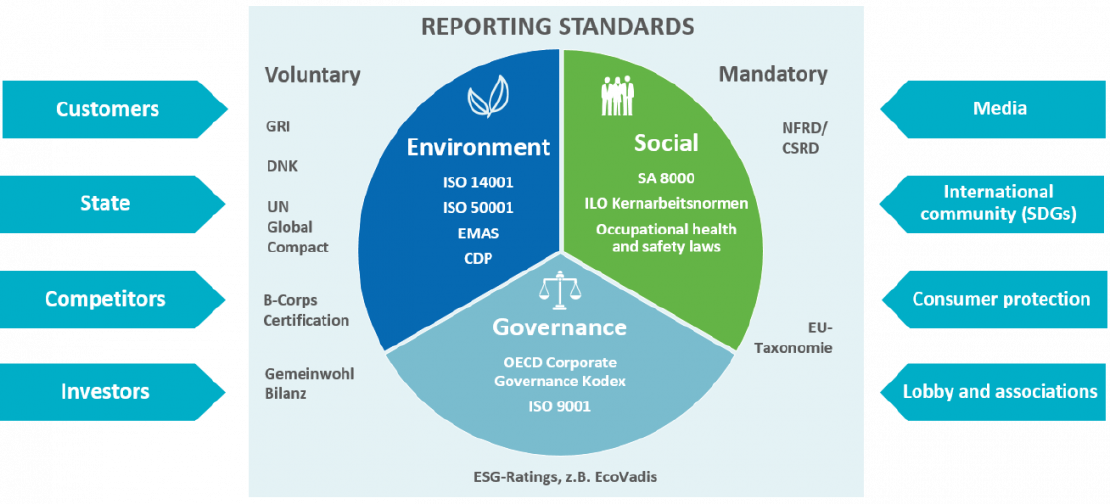

The European Union (EU) has developed a framework for corporate sustainability reporting that aims to promote transparency and consistency in reporting on sustainability issues. The framework is based on the EU Non-Financial Reporting Directive (NFRD), which requires certain large companies to disclose information on their policies, risks, and outcomes relating to environmental, social, and governance (ESG) matters.

Under the NFRD, companies must report on the following areas:

Environmental matters, including the impact of the company’s activities on the environment, its use of energy and natural resources, and its efforts to reduce greenhouse gas emissions.

Social matters, including the company’s impact on its employees, customers, suppliers, and local communities, as well as its efforts to promote diversity and inclusion.

Human rights, including the company’s policies and practices on human rights, such as its approach to labor rights, non-discrimination, and freedom of association.

Anti-corruption and bribery, including the company’s policies and practices to prevent corruption and bribery.

The NFRD applies to all large companies that are listed on EU stock exchanges and have more than 500 employees. Companies that are not listed on EU stock exchanges are encouraged to follow the reporting requirements voluntarily.

In addition to the NFRD, the EU is currently working on a new sustainability reporting standard, which aims to harmonize sustainability reporting across the EU and ensure that companies report on the most relevant sustainability issues. The new standard is expected to be implemented by 2023.

Circular manufacturing or circular economy is defined as a production and consumption model whereby …

With the rising concerns in environmental sustainability, procurement practices are very crucial in driving …

In our quest for sustainable development, it is crucial to understand the environmental impacts of products …